1. Americans Rely on Debt for Survival, Not Luxury, New Surveys Reveal

Millions of Americans are increasingly relying on credit not to fund lavish lifestyles, but simply to afford basic necessities and unexpected emergencies, according to recent financial surveys. Four years after inflation reached its peak, the lingering strain on household budgets continues to force consumers into borrowing just to survive.

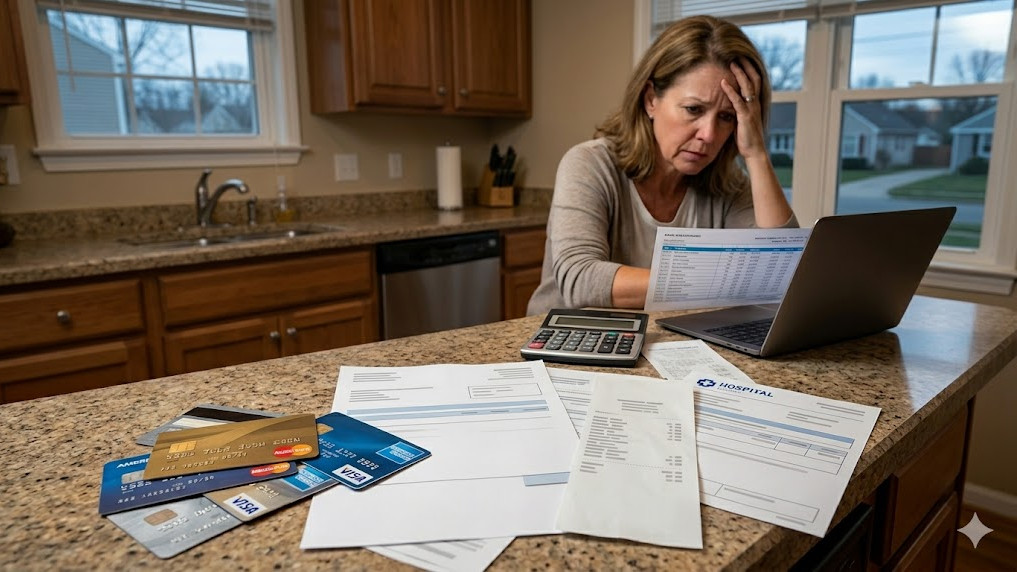

A recent survey conducted by YouGov reveals that 58 percent of Americans currently hold some form of debt, including credit cards, mortgages, or auto loans. Notably, more than 44 percent carry unsecured debt, with a quarter of those individuals owing upwards of $10,000.

The macroeconomic scale of this borrowing is historic. According to data from the Federal Reserve Bank of New York, total US household debt reached a staggering $18.8 trillion by the fourth quarter of 2025, with credit card balances alone accounting for $1.28 trillion.

Rather than discretionary spending, consumers are swiping cards for daily survival. Respondents cited groceries, utility bills, rent, and sudden medical or vehicle repair costs as the primary drivers of their debt. A 2026 report by Bankrate echoes these findings, showing that 41 percent of individuals with credit card debt fell behind due to unexpected expenses, while 33 percent accumulated balances paying for day-to-day living costs.

Financial experts point to the compounding effects of inflation since 2022, which has severely eroded purchasing power. With savings depleted, reliance on credit has become a necessity for many. Current polling indicates that only 30 to 47 percent of Americans can comfortably cover a $1,000 emergency expense out of pocket.

As a result, delinquency rates are steadily climbing. Economists are expressing growing concern for lower-income households, who bear the brunt of elevated living costs. The latest data paints a stark picture of the modern American economy for a growing portion of the country, accumulating debt has become a fundamental tool for everyday survival.

A recent survey conducted by YouGov reveals that 58 percent of Americans currently hold some form of debt, including credit cards, mortgages, or auto loans. Notably, more than 44 percent carry unsecured debt, with a quarter of those individuals owing upwards of $10,000.

The macroeconomic scale of this borrowing is historic. According to data from the Federal Reserve Bank of New York, total US household debt reached a staggering $18.8 trillion by the fourth quarter of 2025, with credit card balances alone accounting for $1.28 trillion.

Rather than discretionary spending, consumers are swiping cards for daily survival. Respondents cited groceries, utility bills, rent, and sudden medical or vehicle repair costs as the primary drivers of their debt. A 2026 report by Bankrate echoes these findings, showing that 41 percent of individuals with credit card debt fell behind due to unexpected expenses, while 33 percent accumulated balances paying for day-to-day living costs.

Financial experts point to the compounding effects of inflation since 2022, which has severely eroded purchasing power. With savings depleted, reliance on credit has become a necessity for many. Current polling indicates that only 30 to 47 percent of Americans can comfortably cover a $1,000 emergency expense out of pocket.

As a result, delinquency rates are steadily climbing. Economists are expressing growing concern for lower-income households, who bear the brunt of elevated living costs. The latest data paints a stark picture of the modern American economy for a growing portion of the country, accumulating debt has become a fundamental tool for everyday survival.